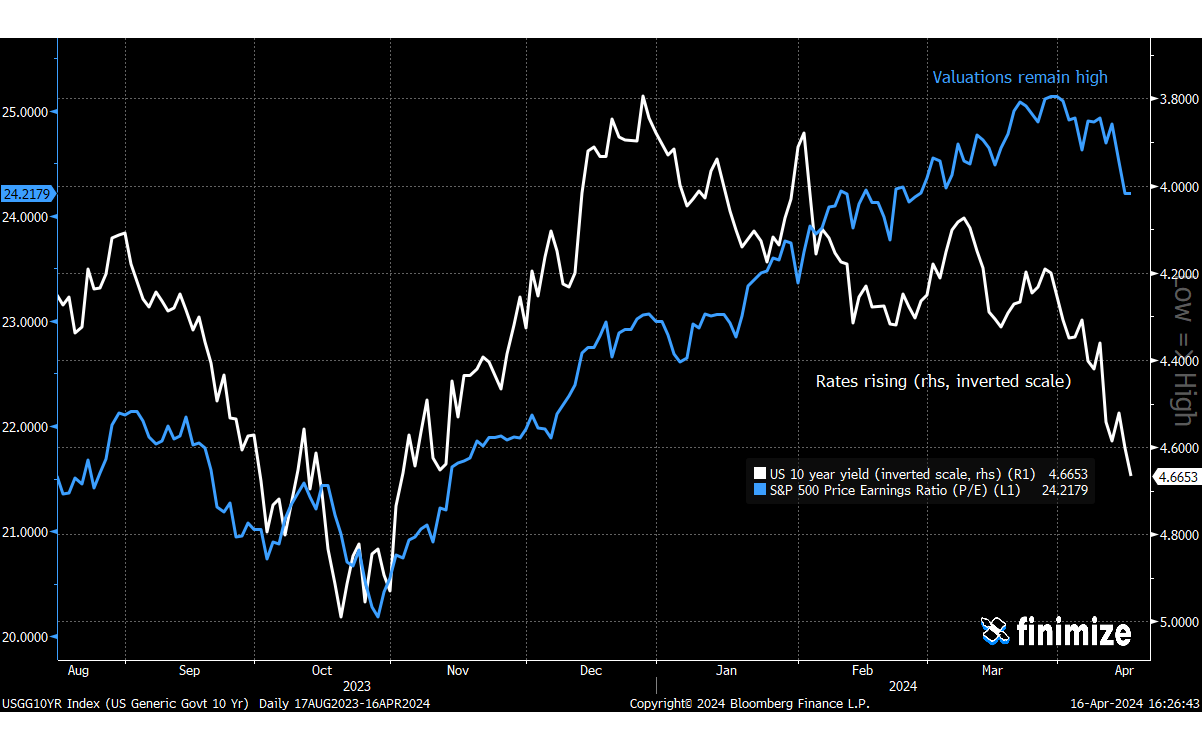

Stocks have been on the up since last October, catapulted mostly by valuation multiples (think: price tags based on earnings) that have soared from 20x to 25x (blue line).

The climb in stock valuations began as interest rates started to dive from 5% to below 4% during a few short months last year (white line, inverted scale on the right-hand side). Lower rates boost the worth of future earnings, so that made total sense. But here’s the twist: rates eventually started to creep higher again this year, and valuations actually crept higher with them – instead of taking the nosedive you’d have expected.

Why, you ask? Well, the economy’s been surprisingly sturdy, even in the face of these higher rates, and that’s allowed investors to focus more on the sunny side of things – like the resilient US consumer and potential earnings growth fueled by AI. And that’s helped to shrug off the drag from those stiflingly high rates.

But that might not last forever. Interest rates tend to have a breaking point where they really start to impact valuations and, by extension, stock prices. And investment bank Morgan Stanley says that point is at the 4.35% yield on the 10-year Treasury.

Interestingly, we’ve just crossed that line. So if interest rates continue to rise, you could expect investors to switch gears and start factoring those higher rates into their valuations, dialing down those multiples. This could spell trouble, not just for lower-quality stocks like small-cap and value stocks – which are even more sensitive to interest rates because of their higher financing costs and riskier balance sheets – but also for the big players, especially if they don’t fully meet investors’ lofty earnings targets.

So as we dive into earnings season, keep one eye on the earnings themselves and the other on where interest rates are heading. They might start to matter a lot more again – and maybe sooner than you think.